The new housing market in Poland: a review of 2019

It seems that this year developers will have sold roughly the same number of units as last year, with the total value of sales contracts definitely set to exceed that of 2018.

This year, however, has not only been good for developers; it has also been a successful year for bankers granting an increasing number of mortgage loans, despite the fact that margins added to the base interest rate have also slightly increased. Politicians will undoubtedly stress the fact that for the first time in the history of post-communist Poland, the number of completed housing units may exceed 200,000. In the country’s major cities there will probably be record numbers of housing units, which will be an opportunity for local authorities to boast of their developer-friendly policies. However, in reality it is difficult to find cities where the local government actually supports new residential developments. Buyers may not view this year as positively, due to increased prices and fewer housing choices.

Certainly, a few things on the primary housing market could have gone worse this year. We could have witnessed the adoption of at least one act significantly affecting price increases and making life difficult for developers. The ruling of the European court regarding Swiss franc loans could have been different, making bankers' lives much more difficult. There may also have been some tax changes that could have negatively affected middle-class buyers - a key group.

Let's briefly recall the most important factors affecting the market environment, and this year’s figures.

Avoiding regulatory turmoil

After the turmoil of the local government elections, politicians returned to working on new laws at the beginning of the year. The industry was hopefully awaiting an amendment to the law regulating agricultural land trade. Restoring the possibility of buying agricultural land without restrictions within city borders would increase the supply of investment sites and maintain the housing supply in the following years. The outcome of the parliamentary debate on the protection of agricultural land turned out to be disappointing from the developers' perspective. Agricultural land turnover within city limits was not completely restored, although the area limit was increased to 1 ha, which was definitely a change for the better.

What was worrying, however, was information about planned amendments to the Act on the Protection of Buyers' Rights and the new Act on Spatial Planning. Ultimately, no new version of the Development Act, which would involve the creation of a Development Guarantee Fund, was adopted, nor was the Act on Spatial Planning, which would introduce completely new planning solutions.

The beginning of October brought a long-awaited ruling from the CJEU regarding Swiss franc loans. Although it was considered ground-breaking from the borrowers’ perspective, in practice it was left to the Polish courts to decide on specific loan agreements. For the banking sector this means that potentially negative effects will be spread over a fairly long period, and there is no indication that this will pose a threat to future lending activity, either for housing buyers or developers. However, this will probably be one of several reasons for an increase in the price of loans over the few next quarters.

Stable demand but not in all segments

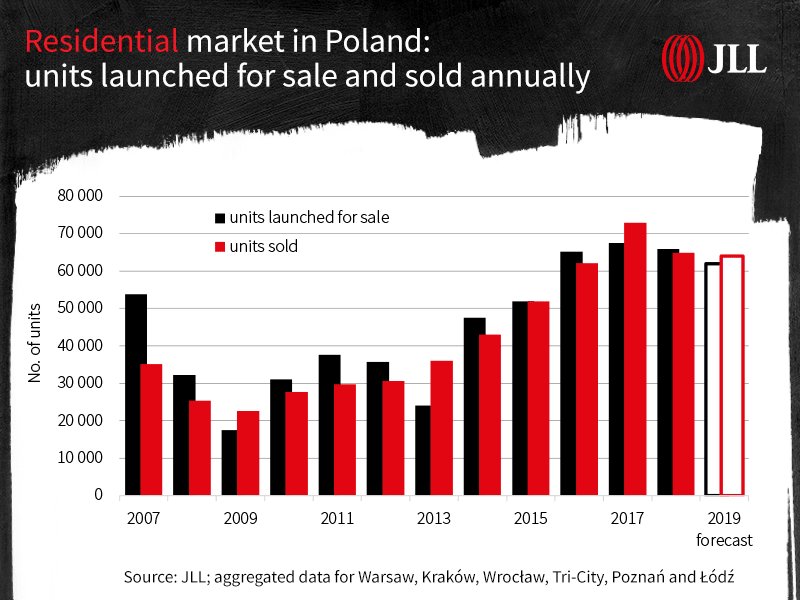

In the six major cities on the real estate market, developers sold 48,000 units by the end of September. The total number of transactions on those markets for the entire year will probably be around 64,000-65,000. Sales records will be set in two cities: Poznań and Łódź. Warsaw will not see record sales, but will end the year with a surplus of sales over new supply. However, on other markets, the differences between the new supply and the number of transactions have so far been less pronounced. The fourth quarter may play an important role in these cities' end of year results.

Demand for housing remained high, although in some market segments interest has already significantly dropped. This was especially visible in the case of flats intended for short-term rental in Gdańsk. At the same time, with continued low interest rates and limited possibilities of investment alternatives, the share of buy-to-let transactions has remained at a level similar to that of last year.

The importance of buyers from the second baby boom is growing

There is a noticeable decline in the share of young buyers taking out a loan to purchase their first flat. This is the result of the "demand shadow" created after the end of the MdM (Housing for the Young) programme, which encouraged this group of buyers in 2017 to make the most of government subsidies. Demographics also play a role here with fewer numbers of university graduates expected over the next few years. This group is also heavily dependent on mortgage loans and on savings from their own equity. So as prices rise, it is increasingly difficult for them to take out a loan. You can also see the phenomenon of young buyers, especially singles, being squeezed out of the market by investment buyers who are looking for the same types of units and can accept higher prices . Finally, this group is moving on to the secondary market, which offers more and more units bought 10-15 years ago by the previous generation, who are now increasingly considering purchasing larger units.

Of course, this change is also a result of demographics. The second baby boom, i.e. buyers born in the years 1976-1985, are in the phase of having more children, choosing schools for their offspring, promotion and professional development, and, unfortunately, in many cases - divorcing. Each of these factors have had a positive impact on housing demand. When it comes to families with children, demand is also slightly supported by the Family 500+ programme, although banks still do not treat these new child allowances as a stable source of income that is taken into account when calculating creditworthiness. Notably, the growing importance of this group of buyers also means, of course, an increase in interest in larger two- and three-bedroom units.

Seniors are aware of the possibilities, Ukrainians intend to stay

The importance of buyers from the older age group is also starting to grow. Post-war baby boomers are about to retire. Some of them can afford a new flat, better suited to the needs of active seniors. The importance of this group on the market will also increase significantly in the coming years. There have also been the first attempts to create an offer for the less active senior customers who are often less aware of the opportunities on the market. In the autumn of this year, construction began in Poznań on one of the largest senior complexes to date that combines care services with an offer for fully independent seniors.

Another observation that is also worth mentioning is that the share of Ukrainians purchasing flats is growing. This is a positive phenomenon, as these immigrants to Poland who first lived in rented accommodation, now look to put down roots by purchasing flats.

The challenges for developers are mounting

For companies and some cities, the decline in sales in the past year was mainly due to the lack of supply, and not due to difficulty in finding buyers. In the first three quarters of the year, developers launched slightly more than 46,000 units for sale in the six major cities on the market, 2,000 fewer than they sold in the same period last year. If the trend from the first three quarters continues, new supply will be approx. 61,000 -63,000 units for 2019.

It is key for companies now to acquire investment plots for reasonable prices and then obtain a building permit within the legal deadline. Fortunately, the increase in construction costs has slowed down, although we will soon be facing new energy saving regulations.

From January 2021, building permits will be issued only for projects that meet the requirements for NZEB, i.e. nearly zero energy buildings. This obviously means an increase in implementation costs. Certainly, many companies will try to obtain, by the end of 2020, a "reserve" of building permits for future projects, which can be started not only in 2021, but in the following two or three years as well.

In view of the modest size of land banks, we will probably see an increase in demand for plots in the first half of 2020, especially in areas covered by local plans or with valid WZ planning decisions.

Meanwhile, there is no change in the reluctant attitude of local governments to enact the Special Act Law Housing, which was supposed to facilitate the acquisition of land for new investments. Some cities are also in the process of developing new studies of conditions and directions of spatial development, an equivalent of master plans for cities in the Polish planning system. Therefore, the cities have limited capacities to get involved with proceedings regarding new local plans. Reserves of partially developed development areas in the central areas of cities are most often post-industrial areas, such as Wolne Tory in Poznań or the Young City in Gdańsk. Investments in such areas are associated with above average costs, which must affect prices.

If not flats, then what?

In the past year, the additional phenomenon that helped strengthen the market in 2018 was still clearly visible. When there was a shortage of areas where ordinary housing units could be built, more and more companies were using their plots designated for commercial functions for different types of quasi-residential investments. They used these locations to build dorms, condo hotels or micro apartments. In all likelihood, the private dormitory market trend will continue. In major Polish cities there are not enough student dormitories, especially since the number of foreign students is rapidly growing from year to year. On the other hand, there is no shortage of foreign funds interested in buying newly built student housing.

However, the future of aparthotels and the short-term rental sector is unclear. At the end of September, The Office of Competition and Consumer Protection (UOKiK) and the Polish Financial Supervision Authority (KNF) issued warnings directed to persons investing or intending to invest in condo- and aparthotels. UOKiK drew attention to the risk of losing funds in the event of the developer's bankruptcy, an uncertain return on investment, as well as the often-opaque relationship between the developer, the intermediary and the consumer. It is difficult to determine to what extent the UOKiK will be able to decrease the demand in the condo hotel sector, but some potential buyers may shift their interest to ordinary flats for rent as they are perceived as a safer investment.

On the other hand, local governments, housing communities, the media and the hotel industry are calling for the regulation of short-term housing rental sector in city centres. Although in Poland this trend is much smaller, compared to Barcelona, Paris or Berlin, one has to take into account some form of limiting the number of units rented in this mode or reducing rental profitability. However, for most developers, demand for such housing does not significantly impact their businesses.

Reserves in demand

In previous years, flexible supply has proved to be a stabiliser in preventing price increases. Currently, prices are rising not only because the costs of production are increasing, but also because, with the still high demand, many companies that do not have a reserve of units for sale are raising prices to slow down their sell-out rate. They have no guarantee that they will be able to complete all the required procedures and preparations within a reasonable time to launch new investments. In a way, it goes against what happened in the past when the primary goal of companies was to sell off all units as fast as possible.

What will 2020 be like?

The outlook for 2020 is still good. Low interest rates with clearly higher inflation will continue to stimulate investment purchases, while mortgages will remain relatively available. There is no threat of excess supply over demand, although the record-high supply in Poznań and Łódź will definitely act as a brake on price increases.

Companies operating on the Polish housing market are aware that sales numbers cannot always be high, and the impending economic slowdown will lower demand for housing. However, the situation of development companies as an industry seems quite secure. The developer sector's resilience to a crisis is associated with two factors: the low debt of developers in the banking sector and high sales. Low debt is the result of banks financing the construction process primarily through granting individual mortgage loans to buyers, which are paid during the construction process to escrow accounts for a given investment, and not through direct financing of developers' activities. Another factor protecting developers from the crisis is high sales numbers, whose gradual drop will not threaten the financial liquidity of businesses. It is more likely that developers will accept a slower sales pace rather than lower prices and will be able to defend their margins.

The economic situation and new regulations will be key for the future of the market over the next few years. While the former depends primarily on global phenomena, the latter depends on the current political situation in the country. Staff changes in the housing and spatial planning department bring about uncertainties regarding whether and what kind of adjustments in the housing policy we can expect during the current parliamentary term. Will the proposed idea of including private development companies in the Housing PLUS programme result in access to land held by the Treasury? Will the government come back to the idea of a Developer Guarantee Fund? Is it realistic to expect housing REITs in Poland? And can a new act on spatial planning be adopted in the near future?

Regardless of what legal changes await us, when thinking about the future we must remember that, compared to 2013, the number of transactions at the peak of the boom, i.e. in 2017, more than doubled. A decrease in demand by one third during an economic slowdown would not be surprising in this situation, and would mean achieving similar numbers to 2015, which was quite a good year. Everything still points to the most likely scenario that the turnover on the primary market will drop at a relatively leisurely pace, which will allow developers to adapt to the changing market situation. Unless something very unfavourable happens in or to the market, there is no threat of a growing disparity between increasing supply and falling demand.

[1] This article was written in mid-December, final data from the monitoring of the housing market for all of 2019 will be published on 23 January 2020.